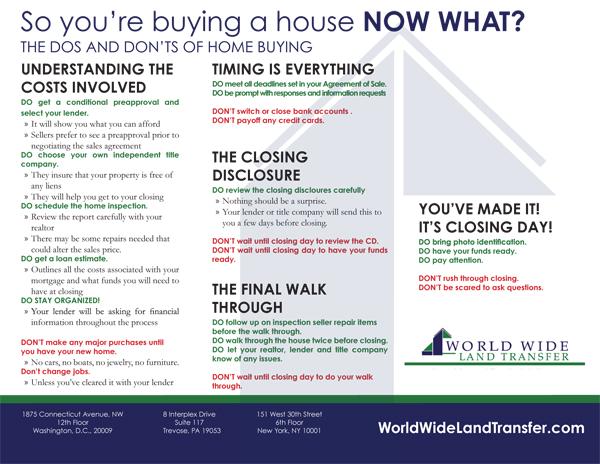

This may be the largest and most important purchase you make during your lifetime. You should be aware of certain rights before you enter into any loan or real estate agreement.

Below you will find some brief information on RESPA (the Real Estate Settlement Procedures Act) and the protections it creates for home buyers and borrowers. We have made more resources available on our page – Consumer Protection & RESPA

Learn

Not certain about their rights! Right after or before you place an offer on a property be sure to contact a Title Insurance professional. If you wait too long, you may find yourself with little choice but to go with the recommendation of your realtor or bank, which will undoubtedly cost you more in closing costs.

Don’t waive your right to choose your own Title Insurance Company. Not all title insurance companies have the same fee structure, regardless of what your realtor or lender might have told you.

You are not obligated to use your real estate agent or lender’s in house company for title insurance.

Avoid getting hit with additional fees at the settlement table by an “in house” operation. Shop around your title insurance just like you do your mortgage! Compare quotes and ask for a complete list of any additional fees in writing. Ask about discounts for which you may be eligible.

You have the RIGHT

Keys to Guarantee A Smooth Settlement